Redlining a Top Priority in 2024

by Leanne Minghini, CRCM, FLE

In 2024, the focus on redlining by regulators remains a top priority, and financial institutions nationwide continue to bear the responsibility of managing redlining risks. Redlining, a discriminatory practice, happens when lenders do not provide credit to individuals living in predominantly minority communities. Recent settlements serve as a strong message that redlining will not be tolerated.

Let’s examine some of the cases that have emerged in 2023 and 2024.

In the last quarter of 2023, the U.S. Department of Justice (DOJ) reached two settlements with lenders as part of its Combatting Redlining Initiative, which commenced in October 2021.

Washington Trust Company of Westerly agreed to pay $9 million to resolve allegations of redlining in predominantly Black and Hispanic neighborhoods in Rhode Island.

Ameris Bank Similarly announced a separate $9 million agreement with Hispanic neighborhoods in Jacksonville, Florida.

The complaints in both cases share similar allegations. The DOJ claimed that Washington Trust Company, between 2016 and 2021, failed to establish a branch in any majority-Black and Hispanic neighborhood in Rhode Island, despite expanding its operations throughout the state. Additionally, the complaint alleged that other banks received nearly four times the number of loan applications each year from majority-Black and Hispanic neighborhoods in Rhode Island during the same six-year period. Furthermore, even when Washington Trust Company did receive loan applications from these neighborhoods, the applicants themselves were disproportionately white.

Ameris Bank, in comparison to their peers received three time less loan applications from majority-Black and Hispanic neighborhoods.

First National Bank of Pennsylvania (FNB) settled with the U.S. Department of Justice and North Carolina for $13.5 million to address allegations of redlining in the Charlotte and Winston-Salem markets in North Carolina.

- The accusations against FNB and the former Yadkin Bank (acquired by FNB in 2017) involved the avoidance of home loans and mortgage services in neighborhoods where the majority of residents were Black and Hispanic between 2017 and 2021.

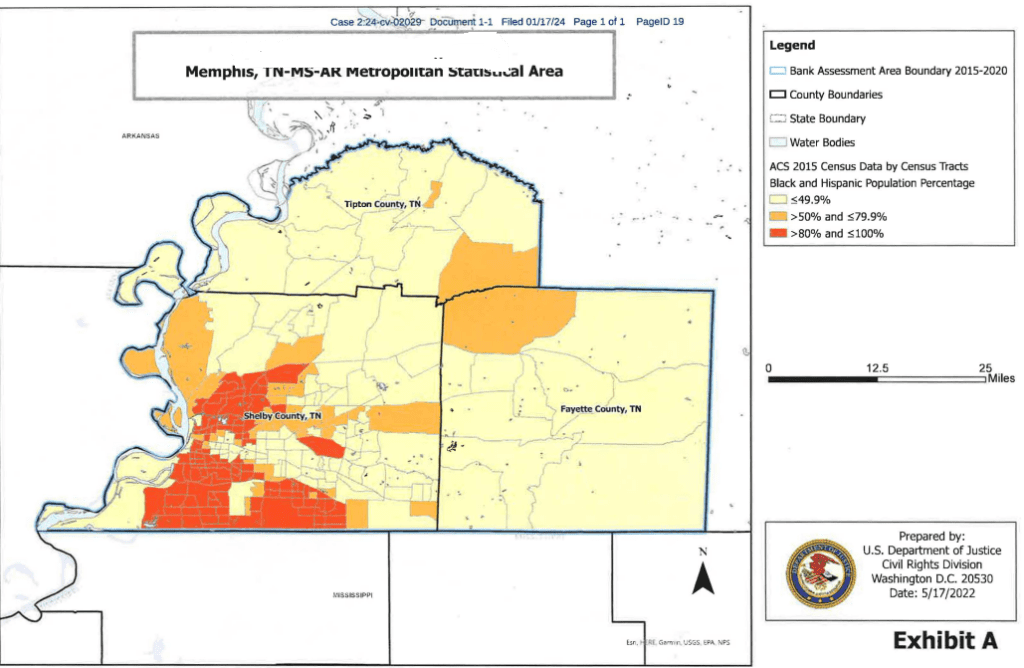

Patriot Bank agreed to a $1.9 million settlement to resolve claims of lending discrimination through redlining in majority-Black and Hispanic neighborhoods in Memphis, Tennessee.

These instances highlight the significance of combating discriminatory practices and advocating for fairness in lending. The Department of Justice remains committed to addressing redlining through its Combatting Redlining Initiative.

Most institutions do not intentionally engage in redlining. It can occur inadvertently due to underwriting standards, marketing practices, product offerings, branch distribution, or the focus of loan officers.

A crucial aspect of preventing redlining is the ability to comprehend where lending activities are concentrated within your institution. If an internal assessment reveals a significant disparity in applications and approvals in majority-Black and Hispanic neighborhoods, it is essential to take corrective action promptly.

- Enhance engagement with the communities within your service areas. It is essential for loan officers to establish connections and increase visibility by actively participating in community events. Merely staying in the office will not yield the desired outcomes.

- Engage branch and compliance personnel in community initiatives. Collaborate with local chambers of commerce and schools to provide financial education workshops and seminars for first-time home buyers.

- Establish connections with real estate agents selling properties in the MMCTs, ensuring compliance with regulations prohibiting kickbacks.